8 Ways to Reduce Chargebacks

By Sydney Vaccaro

As a merchant, chargebacks can eat away at your bottom line, require time and effort from your employees, and damage customer relationships. While the chargeback process is in place to protect consumers from fraud and dishonest merchant interactions, it holds merchants accountable until they prove otherwise. Even if the chargeback is invalid and the merchant is in the right.

So how can merchants retain hard-earned revenue and maintain good customer relationships? The first step to preventing chargebacks is understanding the different types. Typically, chargebacks are broken down into the following categories:

• Friendly fraud: This is when a customer intentionally or accidentally disputes a charge to get their money back. Occasionally, they are simply experiencing buyer’s remorse or attempting to get a refund while keeping the product. Other times, a consumer doesn’t recognize a valid charge on their statement because the business operates under a different name, or the customer simply forgot about the purchase.

Because the customer does not have a valid reason to dispute the charge, merchants can respond to the chargeback with a response document. If the merchant provides the necessary evidence in their response, they will be able to regain their revenue. While it is worth it for merchants to respond to chargebacks, creating response documents can be time and labor intensive. (Retail e-commerce merchants in particular know this song and dance all too well. As more consumers have switched to online shopping due to the COVID-19 pandemic, friendly fraud has reached new heights.)

• Legitimate product issue: This occurs when a customer orders a product and is dissatisfied with it. This can include the product arriving broken, not as described, or not being delivered at all. Instead of using the typical refund process, or perhaps after being denied a refund, the customer will attempt to get the funds back by starting the chargeback process.

• True fraud: This is perhaps the most easily understood type of chargeback. A customer will notice fraudulent charges on their card because their information or the card itself was stolen. These charges were not made by the customer, and the customer often does not receive the goods or services purchased. The fraudsters may keep the items themselves, or they may simply have been testing the card before going on to use the information for other purchases. No matter the reason, the merchant is liable for fraudulent charges and will not be able to regain revenue lost to this type of chargeback.

• Duplicate charge or system issue: Occasionally, human error or a technical glitch can result in a customer being charged multiple times for the same purchase, or for the wrong amount. If these issues are not easily resolved with your customer service team, the customer can turn to their bank to fix the problem.

Not only do chargebacks result in lost revenue, but they can also create issues in securing agreements and partnerships with creditors and financial institutions. In some cases, merchants with a higher than acceptable rate of chargebacks may find themselves with limited banking and processing options. For reference, a chargeback ratio of 1% is considered by many to be the standard threshold.

A high chargeback ratio can result in various requirements being handed down to merchants, such as:

• Cash reserves: If you have a high chargeback ratio, your bank may require you to keep a percentage of your transaction volume aside to cover potential losses which impacts your revenue and cash flow.

• Denial of processing privileges: Some partners may decide it’s too risky to allow you to process credit card payments at all, which is a massive blow to your business.

• High-risk merchant account: A high chargeback ratio could get you placed on the MATCH (Member Alert To Control High-risk merchants) list. As a result, you will be required to pay a premium for services from any payment processor or financial institution.

So how can merchants reduce chargebacks to protect their profits and businesses?

8 Ways to Reduce Chargebacks

The good news is that proper preparation and solid business practices can help you prevent chargebacks in most scenarios. If you are not already following these best practices, consider how you can quickly implement them to improve your bottom line and keep customers happy.

1. Ensure customers are aware of how the transaction will appear: Sometimes, friendly fraud happens because your customer does not recognize the charge on the statement. This can happen if, for example, a larger parent company name appears on the statement, or the official business name is different from what customers are familiar with. For example, H&M is a popular multinational retailer based in Sweden. Customers familiar with the name still might not recognize “Hennes and Mauritz”, which is what H&M stands for. In these cases, merchants should make sure that their merchant descriptor matches the name the public is familiar with.

2. Employ fraud filters and risk management: Since merchants are unable to regain revenue lost to true fraud, it’s vital for merchants to set fraud filters and risk management processes in place. Fraud filters use algorithms to determine whether an order is genuine and stop potentially fraudulent purchases from processing.

An example of a fraud filter is an address verification system or AVS. The cardholder billing address is compared to the address on file with the card issuer. Merchants are advised to only accept transactions with matching AVS responses and automatically decline those that do not match. Merchants can use algorithms and manual checks by humans as part of risk management, whatever is the most effective for your company.

By building out a robust fraud management process you will stop fraud losses from eating away at your bottom line.

3. Clearly stated and flexible refund policy: In general, processes that will help prevent chargebacks will also improve your customer experience. For example, clearly communicating your return and refund policy will prevent unhappy customers and those unhappy customers from trying to submit a chargeback after a failed return attempt.

If a customer requests a refund or needs to know how to return an item, good communication is key. Do not make them wait for a lengthy period, as they may decide to investigate chargeback alternatives.

4. Invest in logistics: Proper logistics and tracking will cut down on customer service calls and chargebacks. By getting your package to your customer on time and undamaged will improve customer experience, cut down on customer service volume, and prevent chargebacks.

Good product tracking is also very important. Customers feel reassured when they can see their product on the way, and you’ll be able to verify if something was delivered and where. This information is also helpful as compelling evidence in a response document if you need to challenge a chargeback.

Investing in logistics is especially important for cross-border e-commerce in China. To learn more, check out this free guide.

5. Write transparent product descriptions: Make sure your product descriptions are complete and accurate. This includes basics like assembly or batteries required to other things your customers should know. Any accompanying photos should be accurate and showcase the product as it is when delivered or assembled. If anything in the photo is different, such as a couch shown with accompanying throw pillows, make sure the description is clear if those items are included. This prevents chargebacks from upset customers who feel the description was deceptive.

6. Provide good customer service: Delivering what you say you will, when you say it will arrive, is part of this. However, your staff will also be responsible for addressing customer inquiries. Make sure they’re trained to be responsive, helpful, and thorough. Good record-keeping for customer accounts is also crucial, and can help identify potential gaps in operations.

7. Invest in continuous research and improvement: Once your processes are in place, make sure you continuously review them and see if there are potential flaws. If you start receiving a lot of chargebacks from customers claiming they never received their refund, look at the time it takes for a refund to hit a customer’s bank account. Use chargebacks or unhappy customer calls as an opportunity to grow.

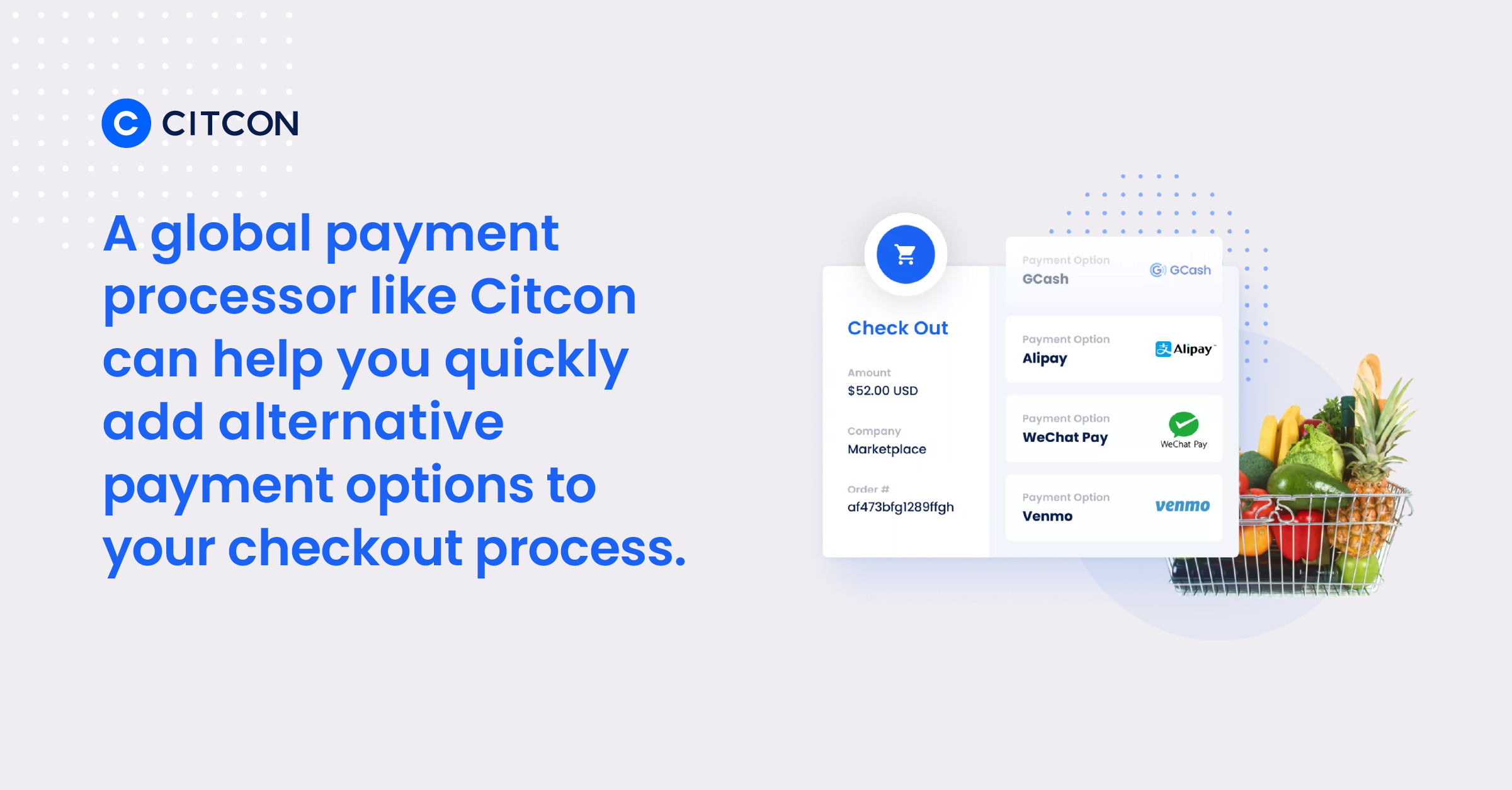

8. Offering the alternative payment methods: Having alternative payment options at checkout can go beyond attracting new customers and improving customer service. It can also help prevent fraudulent purchases and chargebacks from happening. Unlike traditional payment methods, merchants don’t accept chargeback liability with certain wallets. So you can add these payment methods online and in-store without worrying about additional fraud or chargeback liability.

A global payment processor like Citcon can help you quickly add alternative payment options (popular digital wallet brands including PayPal, Venmo, AliPay, WeChat Pay, as well as buy now pay later services, cryptocurrency, and more) to your checkout process. By adding more payment options you can create a more secure checkout experience and delight international and local customers with their preferred payment method.

The steps to prevent chargebacks go beyond shielding your revenue. These processes will improve customer experience, decrease your customer service workload, and so much more. Addressing chargebacks and fraud holistically will put your company on track to not only preserve revenue but increase it.